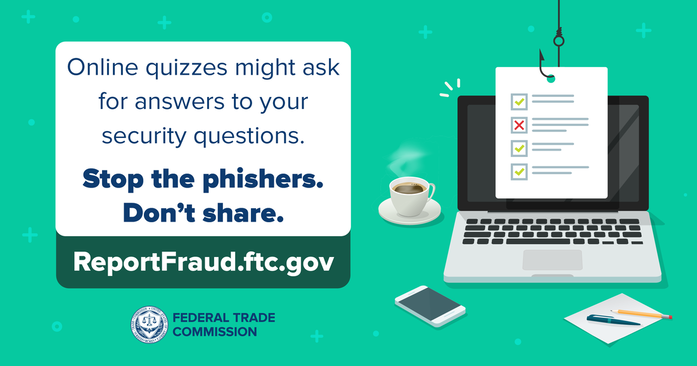

by Amy Kleinschmit, Chief Compliance Officer FTC Warning – Dangers of Online Quizzes The Federal Trade Commission (FTC) shared this consumer alert regarding online quizzes – good reminder for staff and members. As discussed in the alert, “Personality tests, quick surveys, and other types of online quizzes ask seemingly harmless questions, but the more information you share, the more you risk it being misused. Scammers could do a lot of damage with just a few answers that give away your personal information.” The alert discusses that one major way to protect personal information is to steer clear of online quizzes.  Refresher - When is a change of terms notice needed? A reoccurring scenario, the board decides to change fees or change rates and now the credit union must implement these changes. Before we can tackle when a change of terms notice is needed, the first question that needs to be determined is does the agreement/contract allow for changes. For the purposes of this article the focus is on regulatory requirements for change in terms notices and not contractual requirements. Therefore, to know if, and when, a change in terms notice is required the credit union must first identify what regulation is requiring the disclosure of the particular term so we can determine how to comply with changing the term. Unfortunately, each regulation has its own nuances that need to be complied with. Take for example the Truth in Saving Act, found under Part 707 of the NCUA rules and regulations. Section 707.5 covers the requirements for subsequent disclosures and directs that a credit union shall give advance notice to affected members of any change in a term required to be disclosed under § 707.4(b), if the change may reduce the annual percentage yield or adversely affect the member. The notice shall include the effective date of the change. The notice shall be mailed or delivered at least 30 calendar days before the effective date of the change. The commentary to the regulation provides guidance on the form of the notice. Credit unions may provide a change-in-term notice on or with a regular periodic statement or in another mailing (such as a highlighted portion of a newsletter or statement stuffer insert). If a credit union provides notice through revised account disclosures, the changed term must be highlighted in some manner. For example, credit unions may state that a particular fee has been changed (also specifying the new amount) or use an accompanying letter that refers to the changed term. NCUA commentary reminds that - “Credit unions are cautioned that unless credit unions have reserved the right to change terms in the account agreement or disclosures, a change-in-terms notice may not be sufficient to amend the terms under applicable law.” Truth in Savings does include several exceptions which do not require notice, such as variable rate changes (changes in the dividend rate and corresponding changes in the annual percentage yield in variable-rate accounts); share draft and check printing fees; or short-term term share accounts (changes in any term for term share accounts with maturities of one month or less.) Unlike the Truth in Saving Act, Regulation CC – Availability of Funds and Collection of Checks, requires notice of changes in policy both when the change would adversely affect the member and also when the change expedites the availability of funds, or in other words is a positive thing for the member. Under Regulation CC, 229.19(e), the credit union is required to send a notice to holders of consumer accounts at least 30 days before implementing a change to the availability policy regarding such accounts, except that a change that expedites the availability of funds may be disclosed not later than 30 days after implementation. Under Regulation CC, a notice may be given in any form as long as it is clear and conspicuous. If the credit union gives notice of a change by sending the member a complete new availability disclosure, the credit union must direct the member to the changed terms in the disclosure by use of a letter or insert, or by highlighting the changed terms in the disclosure. Electronic Fund Transfers Act, as implemented by Regulation E, adds another layer of compliance to the mix. Section 1005.8 provides that - a financial institution shall mail or deliver a written notice to the consumer, at least 21 days before the effective date, of any change in a term or condition required to be disclosed under § 1005.7(b) of this part if the change would result in: (i) Increased fees for the consumer; (ii) Increased liability for the consumer; (iii) Fewer types of available electronic fund transfers; or (iv) Stricter limitations on the frequency or dollar amount of transfers. With regard to the form of the change in terms notice for Regulation E, no specific form or wording is required. The notice may appear on a periodic statement, or may be given by sending a copy of a revised disclosure statement, provided attention is directed to the change (for example, in a cover letter referencing the changed term). Regulation E does not require change in terms notice when closing some of an institution's ATMs; or for the cancellation of an access device. There is also an exception to the “prior” requirement when an immediate change in terms or conditions is necessary to maintain or restore the security of an account or an electronic fund transfer system. If the credit union makes such a change permanent and disclosure would not jeopardize the security of the account or system, the credit union shall notify the consumer in writing on or with the next regularly scheduled periodic statement or within 30 days of making the change permanent. If the credit union is contemplating a change to a term required to be disclosed under Regulation Z – Truth in Lending, that will require even more careful consideration and review to make sure that the term can be changed – terms of existing closed-end loans generally cannot be changed. With regard to open-end consumers loans, Regulation Z has very specific timing, formatting, and disclosure requirements. Provisions relating to credit cards add even more layers to the mix – which will be a discussion for a future Memo article. However, if the suspense is too much, don’t forget you can find detailed summaries on Reg Z requirements, including change in terms requirements in InfoSight. If you have not requested access to this due support (free) benefit of membership, just select request account to get started now. As always, DakCU members may contact Amy Kleinschmit with any compliance related questions or concerns. Comments are closed.

|

|

Copyright Dakota Credit Union Association. All Rights Reserved.

2005 N Kavaney Dr - Suite 201 | Bismarck, North Dakota 58501 Phone: 800-279-6328 | [email protected] | sitemap | privacy policy |

|

|

|

|